Economics

Economics is one of the social sciences that explains the economic activities of individuals. Any activity related to earning and spending money is considered an economic activity. Almost everyone engages in economic activities because they want to earn money.

The main economic problem is how to transform society's resources into consumable commodities using productive technology. This problem arises because human wants are unlimited while society's resources are limited. Therefore, the central task of economics is to determine how much of which commodities should be produced to achieve the optimum satisfaction of human wants.

Definitions of Economics

The definitions of economics can be classified into four categories:

- Wealth definitions

- Welfare definitions

- Scarcity definitions

- Growth definitions

Wealth definitions

Almost all classical economists followed the definition of wealth, which is primarily associated with J.B. Say and Adam Smith. Adam Smith is often called the "Father of Economics."

According to J.B. Say, "economics is the study of the science of wealth," while Adam Smith states that "economics is the science which deals with wealth."

Main Points:

- Economics explains how wealth is produced, consumed, exchanged, and distributed.

- Adam Smith viewed man as an economic being.

- Economics primarily focuses on the study of wealth.

- This definition addresses the causes behind the creation of wealth.

- It primarily considers material wealth.

Welfare Definition

This definition was provided by Alfred Marshall: "Economics is the study of mankind in the ordinary business of life. It examines that part of individual and social action which is most closely connected with the attainment and use of the material requisites of well-being."

Main Points:

- This definition establishes economics as a social science.

- Goods are classified into two categories:

- Material goods

- Immaterial goods

Merits:

- Economics is a social science.

- Priority is given to human welfare over wealth.

- Marshall emphasized the role of "social man" rather than "economic man."

Scarcity Definition / Robbins' Definition

Lionel Robbins provided this definition in his famous book An Essay on the Nature and Significance of Economic Science (1932). He defined economics as follows:

“Economics is a science which studies human behavior as a relationship between ends and scarce means that have alternative uses.” — Robbins

Main Points:

- Wants are unlimited.

- Resources are limited.

- Resources have alternative uses.

- Economics involves making choices.

Merits:

- Economics is an analytical science.

- Economics is universal.

- Robbins defined economics as a positive science.

- Economics remains neutral between ends.

Growth Definition

This definition was provided by J.M. Keynes and P.A. Samuelson in Samuelson's book, Economics: An Introductory Analysis (1948):

“Economics is the study of how men and society choose, with or without the use of money, to employ scarce productive resources that have alternative uses to produce various commodities over time, and to distribute them for consumption now or in the future among various persons and groups in society. It analyzes the costs and benefits of improving patterns of resource allocation.” — P.A. Samuelson

Main Points:

- Like Robbins, Samuelson acknowledges scarcity and alternative uses of resources.

- Economic issues extend into the future, introducing the concept of a time element.

- Samuelson adopted a dynamic approach, considering economic growth an integral part of economics.

- This definition merges Marshall's welfare definition with Robbins' scarcity definition.

Nature of Economics

In economics, a "want" is something that is desired. A want is the starting point of economic activity. Wants lead to efforts, and efforts lead to satisfaction. Thus, the chain goes: Wants → Efforts → Satisfaction.

The subject matter of economics is divided into four primary areas:

- Production

- Exchange

- Distribution

- Consumption

Production

In economics, production involves creating goods and services by utilizing resources. It is the process of transforming raw materials into final or finished goods, essentially the creation of utility. To produce anything, several essential factors are required. These factors are classified into four categories:

- Land

- Labor

- Capital

- Organization

Technique and Technology

The technique refers to the ratio in which inputs are combined to produce one unit of a product. For example, if capital (K) and labor (L) are used in production, and 1 unit of K is combined with 2 units of L to produce 1 unit of the product, then the ratio K:L = 1:2 is the technique of production.

If additional techniques are known, such as K:L = 2:3 and K:L = 3:4, then these multiple ratios form the technology—essentially, the spectrum of all available techniques.

Exchange

Exchange involves transferring goods from one person to another. Historically, goods were exchanged directly, known as the "barter system." However, to address the limitations of barter, money was introduced. Now, goods are exchanged for money, and price is essential in facilitating this exchange.

Distribution

Distribution refers to the sharing of income among the factors of production. The total income generated by selling goods and services in the market is distributed among the factors of production in the form of rent, wages, interest, and profits.

Types of Distribution

-

Micro Distribution: This involves determining the price of each factor of production. For example, the pricing of land (rent per unit), labor (wages), and capital (interest rates). Theories such as the Ricardian theory of rent, wage theories, interest theories, and profit theories are discussed under micro distribution.

-

Macro Distribution: This refers to the distribution of total national income among all factors of production within society. It examines whether income is distributed fairly or unequally among different groups in society.

Modern economists have expanded the scope of economics to include additional concepts, such as:

- Employment

- Income

- Economic Planning and Development

- International Trade

Consumption

Consumption is the act of using goods or services to satisfy wants. In economics, consumption is typically defined as the final purchase by an individual for personal use, rather than as an investment. For instance, buying food, clothing, or a car for personal use is considered consumption.

However, if a purchase is intended to generate income, such as buying a car to operate a taxi business or purchasing a house to rent out, it is viewed as an investment rather than consumption. Thus, the purpose of the purchase determines whether it is classified as consumption or an investment.

Scope of Economics

Traditional Approach

- Economics is a social science that studies human behavior as a rational social being.

- It is considered a science of wealth in relation to human welfare.

- The earning and spending of income were viewed as the primary goals of all economic activities.

- Wealth is considered a means to an end, with the ultimate end being human welfare.

Modern Approach

An individual, whether as a consumer or a producer, can optimize their goals through economic decision-making:

- The scope of economics lies in analyzing economic problems and suggesting policy measures.

- Social problems can be explained using either abstract theoretical tools or empirical methods.

- In classical discussions, economics is considered a positive science, seeking to explain what the problem is and how it can be solved.

- In modern times, it is regarded as both a positive and a normative science.

- Economists today address economic issues not only as they are but also as they should be.

- Welfare economics and growth economics tend to be more normative than positive.

Scope of Macro Economics

Macroeconomics studies national income, including the calculation of national income and trends in national income. It also examines total employment (full employment), total output, trade cycles, and inflation. Additionally, it explores theories of economic growth and the macroeconomic theory of distribution. This field is also referred to as the theory of income and employment.

Scope of Micro Economics

The Micro economics explains how the price of a good is determined and how the price per unit of factors of production is determined and it is also deals with theories of economics welfare.So Microeconomics is called “Price theory”.

Importance of Economics For Engineers

The following are some of the most crucial functions of engineering economics:**

- Cost Analysis: Engineering economics provides valuable insights into the costs associated with various engineering projects, including labor, materials, and tools. This analysis helps determine the viability of different projects and identifies the most cost-effective options.

- Time Value of Money: Engineering economics takes into account the value of money over time when assessing the profitability of various investment opportunities. This principle is essential for making informed financial decisions.

- Decision-Making: The discipline of engineering economics offers a systematic framework for evaluating the relative merits of potential courses of action. This framework enables informed choices that maximize benefits while minimizing costs.

- Risk Analysis: Evaluating the financial impact of potential risks is another important aspect of engineering economics. This analysis is useful for formulating risk management strategies that minimize adverse effects.

- Project Management: Engineering economics plays a crucial role in managing engineering projects by assisting in the creation of project budgets, estimating costs, and monitoring expenditures. This support helps ensure that projects are completed on schedule and within budget.

- Optimization: By determining which design and operational choices provide the best value for money, engineering economics contributes to the optimization of engineering systems. As a result, engineering projects and systems become more productive and profitable.

Significance of Economics For Engineers

- Informs Decisions: Economists provide information and forecasts to guide decision-making within companies and governments. This knowledge of economics—often referred to as economic intelligence—is based on data and modeling.

- Influences Everything Economic issues impact our daily lives, including factors such as taxes, inflation, interest rates, wealth, inequality, emerging markets, and energy and the environment. As a broad subject, economics offers insights into a range of health, social, and political issues that affect households and communities.

- Impacts Industries: Firms of all sizes and in various industries rely on economics for product research and development, pricing strategies, and advertising. This wide-ranging influence means that studying economics can open up a variety of career options across all sectors of the economy, from agriculture to manufacturing, banking, and consultancy.

- Inspires Business Success: Understanding consumer behavior is vital for a business's success. Economists use theories and models to predict behavior and inform business strategies, including the analysis of "big data."

- International Perspective: Economics affects the world we live in. Understanding both domestic and international perspectives—historical and current—provides valuable insights into how different cultures and societies interact. For international corporations, grasping the dynamics of the world economy is key to driving success

- Significance of Macroeconomics:

- Understanding the Working of an Economy: Macroeconomics helps analyze the overall functioning of an economy.

- Formulating Policies: It assists policymakers in creating effective economic policies.

- Preparing Economic Plans: Macroeconomics is essential for developing comprehensive economic plans.

- Taking Remedial Measures for Trade Cycles and Inflation: It provides tools to address fluctuations in trade cycles and manage inflation.

- Significance of Microeconomics:

- Understanding the Operations of an Economy: Microeconomics focuses on the individual components of an economy, helping to understand how different sectors operate.

- Economic Welfare of People: It analyzes how economic policies affect the welfare of individuals and communities.

- Managerial Economics: This branch applies microeconomic principles to business decisions, optimizing resource allocation and strategy.

Distinction Between Micro and Macroeconomics

Microeconomics

Microeconomics studies the behavior of individual units, such as consumers, producers, firms, or industries.

Alfred Marshall significantly developed microeconomics, emphasizing the division of the economy into small units for detailed study. According to Marshall, microeconomics explains how consumers achieve maximum satisfaction, how producers obtain maximum output, and how firms realize maximum profit.

Definition: Microeconomics is the study of "particular firms, particular households, individual prices, wages, incomes, individual industries, and particular commodities." — K. E. Boulding.

Macroeconomics

The term "macro" is derived from the Greek word "makros," meaning "large" or "very big." Macroeconomics studies the economy as a single unit and does not focus on individual units. Instead, it deals with aggregates, totals, and averages.

For example, it examines national income, full employment, total output, total investment, total consumption, and other broad economic indicators.

Definition: According to Gardner Ackley, “Macroeconomics is concerned with such variables as the aggregate volume of output of an economy, the extent to which resources are employed, the size of national income, and the general price level.”

| Macroeconomics | Microeconomics |

|---|---|

| Output and income, unemployment, inflation, and deflation. | Preference relations, supply and demand, opportunity cost. |

| Used to determine an economy's overall health, standard of living, and needs for improvement. | Used to determine methods of improvement for individual business entities. |

| Top-down approach is the approach of study. | Bottom-up approach is the approach of study. |

| Underemployment of the resources. | Full employment in economy. |

| Economic growth, reducing poverty and income inequality, price stability, trade balance, full employment, etc. | Consumer satisfaction, economic growth, market efficiency, and optimal use of resources, etc. |

| Method of study is general equilibrium analysis. | Method of study is partial equilibrium analysis. |

Concept of Utility and Its Types

Definition

The additional benefit that a person derives from a given increase in their stock of anything diminishes with each increase in the stock that they already have. — Alfred Marshall.

This definition refers to the principle of diminishing marginal utility, which states that as a person acquires more of a good or resource, the additional satisfaction (or utility) gained from each additional unit decreases. For example, the first slice of pizza may provide significant enjoyment, but by the time a person consumes a fifth or sixth slice, the additional satisfaction gained from each extra slice tends to diminish.

The law of diminishing marginal utility (DMU) was first proposed by H.H. Gossen in 1854, making it known as Gossen’s first law of consumption. Alfred Marshall further developed this concept.

Concepts in this Law

Marginal Utility:

Marginal utility is the additional utility gained by the consumer from consuming one more unit of a good or service. It represents the change in total utility resulting from the consumption of that additional unit.

The change in the total utility is also called marginal utility.

or

Total Utility:

Total utility refers to the overall satisfaction a consumer derives from consuming all units of a particular good or service. It is the sum of the marginal utilities of each unit consumed.

Sum of the total marginal utility is called Total Utility.

Or

| Units | Total utility | Marginal utility |

|---|---|---|

| 1 | 40 | 40 |

| 2 | 70 | 30 |

| 3 | 90 | 20 |

| 4 | 100 | 10 |

| 5 | 100 | 0 |

| 6 | 90 | -10 |

Here depicts a table that outlines the relationship between total utility and marginal utility for varying quantities of a good. The first column represents the number of units consumed, while the second column shows total utility values. The third column displays marginal utility, which indicates the additional satisfaction gained from consuming each successive unit. Notably, as more units are consumed, total utility increases but marginal utility decreases and eventually becomes negative after a certain point.

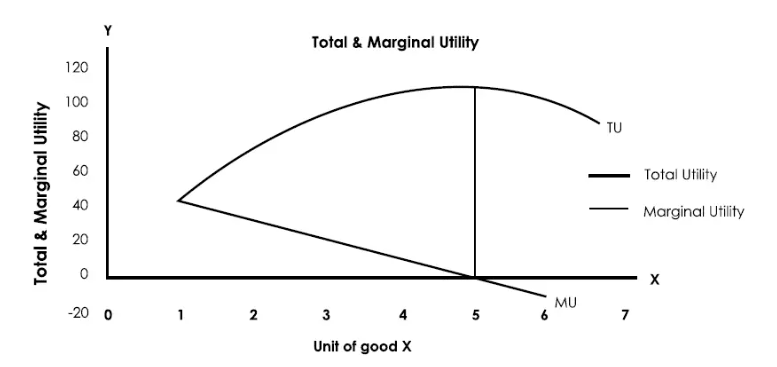

The Diagram shows the concepts of Total Utility (TU) and Marginal Utility (MU) for a unit of good X. The Y-axis represents utility values, while the X-axis indicates the quantity of good X. As units increase, Total Utility rises, while Marginal Utility varies until it decreases. This visual representation helps to understand how consumption affects overall satisfaction levels.

Analysis of the Diagram

- When total utility (TU) increases, marginal utility (MU) diminishes. Therefore, the TU curve slopes upward from left to right, while the MU curve slopes downward. This is true as long as the law of diminishing marginal utility applies. Initially, it is possible for marginal utility to rise alongside total utility for a specific commodity.

- When total utility reaches its maximum, marginal utility is zero. At this point, the TU curve peaks, and the MU curve intersects the x-axis.

- When total utility begins to diminish, marginal utility becomes negative. Consequently, the TU curve slopes downward, and the MU curve crosses the x-axis

Assumptions:

- The units are homogeneous.

- The units must be of reasonable size.

- There are no changes in the tastes and preferences of the consumer.

- Importance of DMU: Value paradox , Basis for economic laws , Finance Minister , Re-distribution of wealth.